The second quarter of 2019 saw an average increase in power generation from wind and large-scale solar by 90MW and 10.9MW respectively. The coal power production dropped by 7% during the peak demand periods of day time. In addition, Rooftop PV contribution jumped to 19.4MW. This increase is mainly due to the number of new installations connecting to the South West Interconnected System (SWIS).

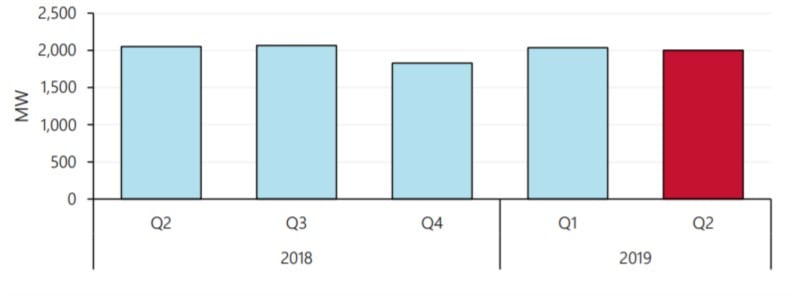

In Perth, the average power demand was 2.5% lower than that in Q2 2018, and the lowest since 2008. Perth had the lowest price ($)/watt for 5kW and 6kW solar system at 0.41 and 0.38 respectively. In WA (mainly the Perth CBD), one in four households have rooftop solar system – a total of 1.1 GW. On the other hand, there was an increase in wind power generation due to optimal meteorological conditions, and due to the connection of the new Badingarra wind Farm (130MW). The minimum energy demand during Q2 2019 was 1,235 MW. This is still higher than the all-time low of 1,173 MW.

Furthermore as a result of increased demand from mineral processing industry, the gas consumption rose to 96.7 PJ – a 12% increase from Q1 2019. The Wheatstone plant had a production hike of 5PJ. The Balancing prices also fell by 7% – lowest being $43.57/MWh. During high process intervals, coal and gas were the largest online sources contributing to 49% and 46% of generation respectively.

During Good Friday (19th April, 2019), the market experienced a fair degree of volatility in demand and pricing. This was mainly because of high variability in wind outputs and lower irradiation from larger cloud covers. The output from rooftop PV systems were variable and reached a maximum of 500MW. The balancing prices were negative for 19 intervals, reaching over 100$/MWh. This was mainly due to the aforementioned variabilities and forecasting hindrances.